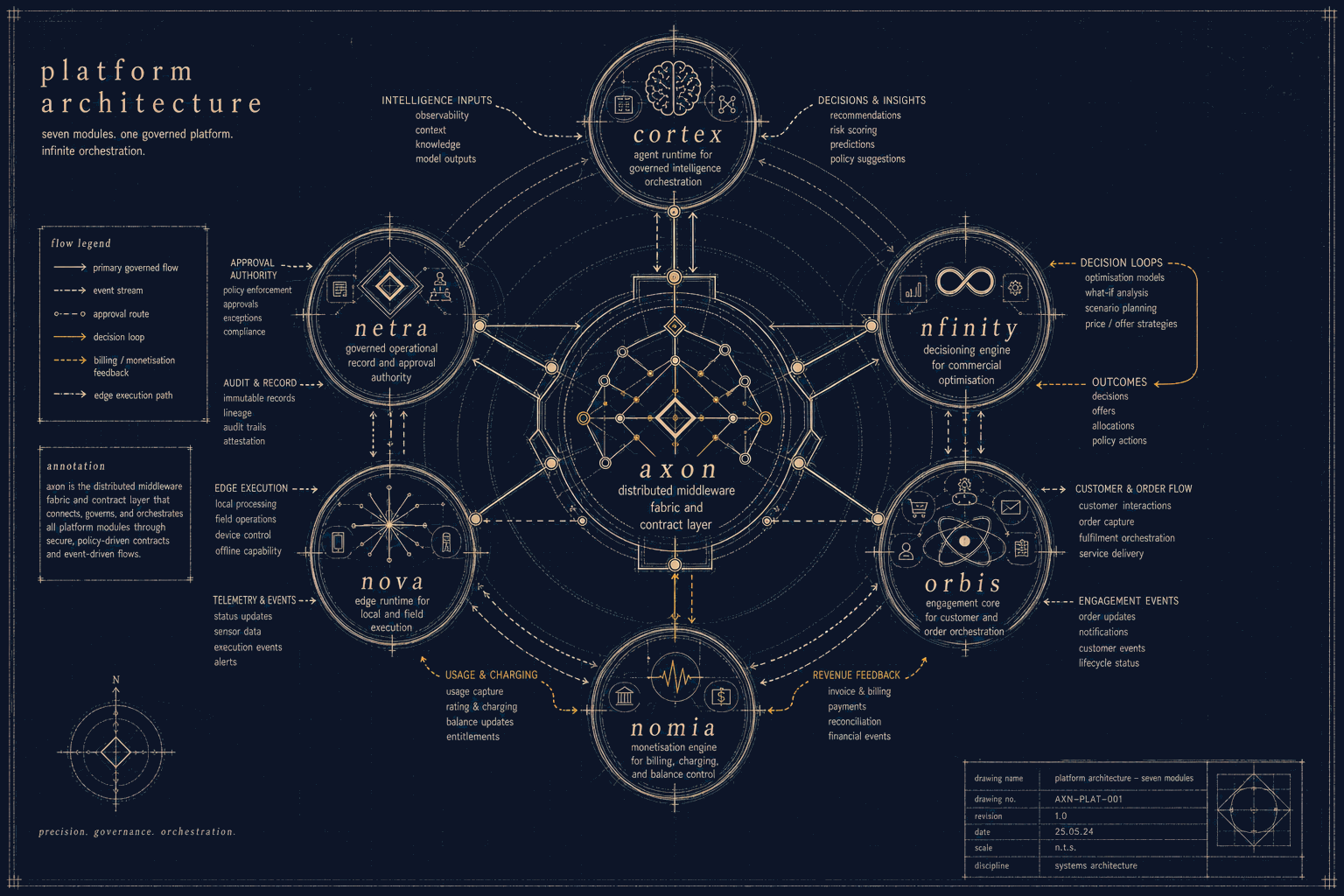

Platform point solutions

Start with the problem the operation has to survive.

Same platform. Different pressure. Different route.

Telecom buyers rarely need another generic platform diagram. They need to know whether the system can carry the operating reality the business actually has: live charging, partner settlement, the next product launch, and the team that has to run it on a Tuesday morning.

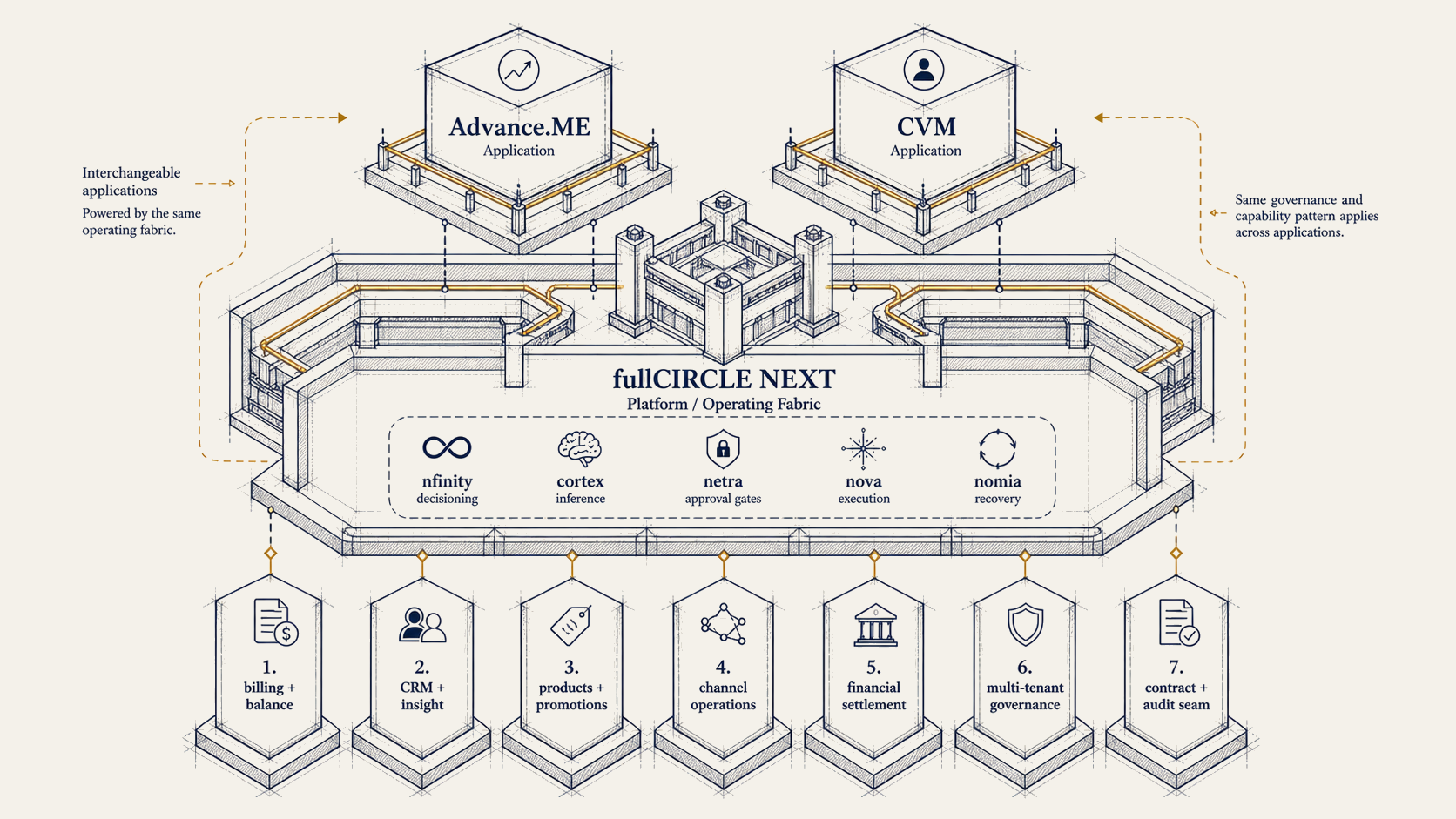

Six buyers, six pressure points. fullCIRCLE NEXT, Advance.ME, CVM, and the advisory practice underneath all stay the same. What changes is the order they show up in and the work they do first.

How to read this page

Choose by the pressure on the operation, not by the catalogue.

A converged operator, a digital MVNO, a bank, a wholesale business, an ISP, and an enterprise channel provider all need charging, BSS, decisioning, integrations, and controls. They do not need them for the same reasons.

What changes is where the work starts, what the platform absorbs first, and which advisory practice walks beside it. The fullCIRCLE NEXT modules underneath stay the same.

Operators

Move the core without shaking the business loose.

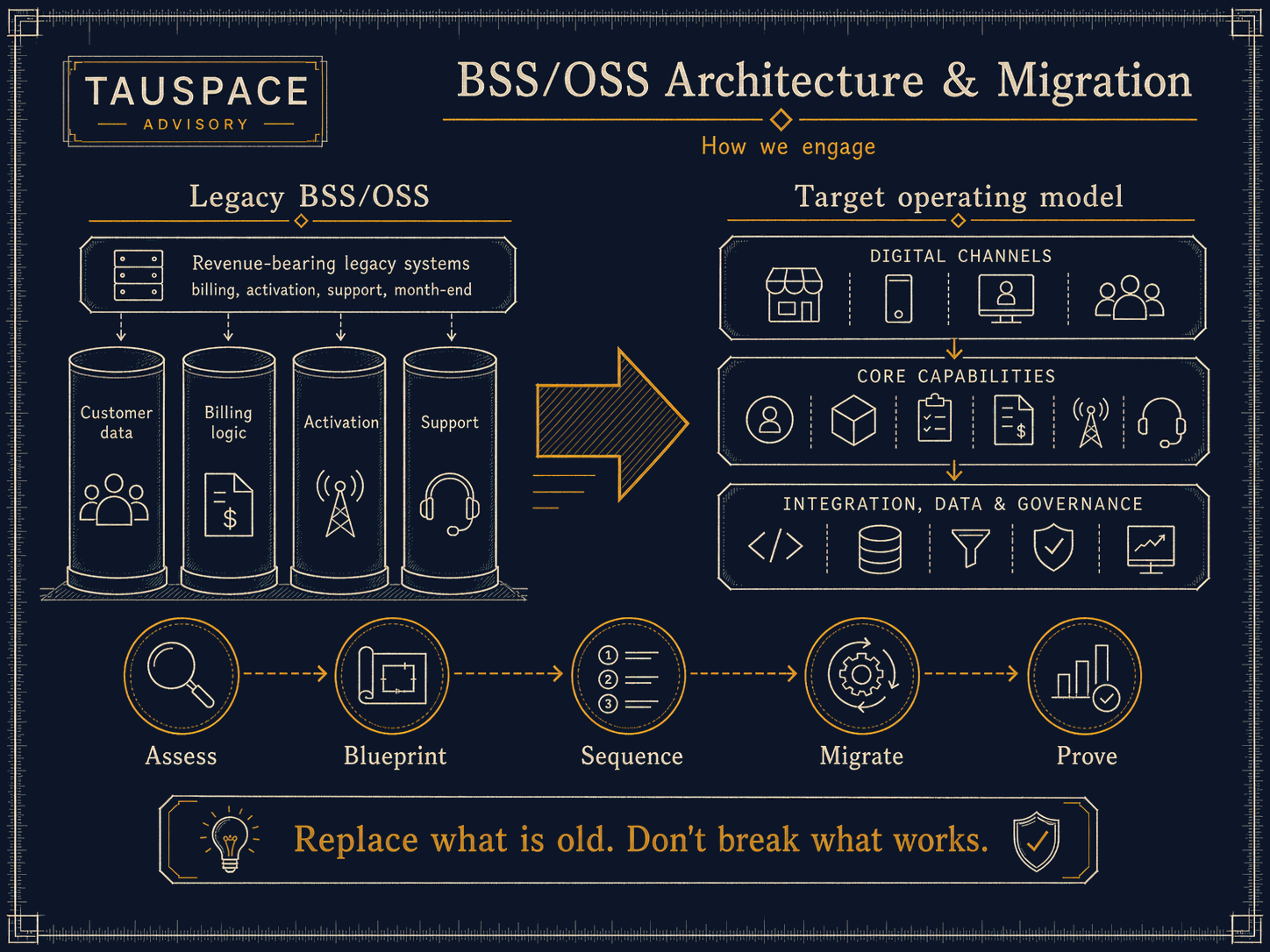

Operators do not get the luxury of rebuilding in a quiet room. The estate has to keep billing, activating, reconciling, and answering the phone while the architecture changes underneath it.

Questions on the table

- Can we modernise charging and BSS without breaking live operations?

- Can the architecture support converged, prepaid, postpaid, wholesale, and digital journeys?

- How do we reduce dependency on brittle custom integrations?

- Where do we start without committing to a risky rip-and-replace?

- How do we prove the migration is controlled before it reaches customers?

What the platform carries

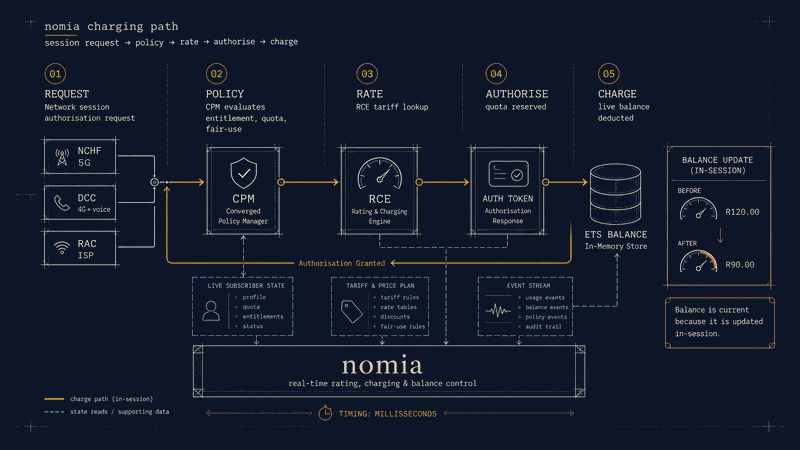

On the operator side, the platform carries the load the legacy stack used to carry, one domain at a time: charging and policy, product and subscriber, decisioning, integration, deployment control, and the evidence that the migration is actually controlled. The aim is not to make the operator fit a product. It is to shape a path that can move through the live estate with clear migration boundaries.

MVNOs and Digital Brands

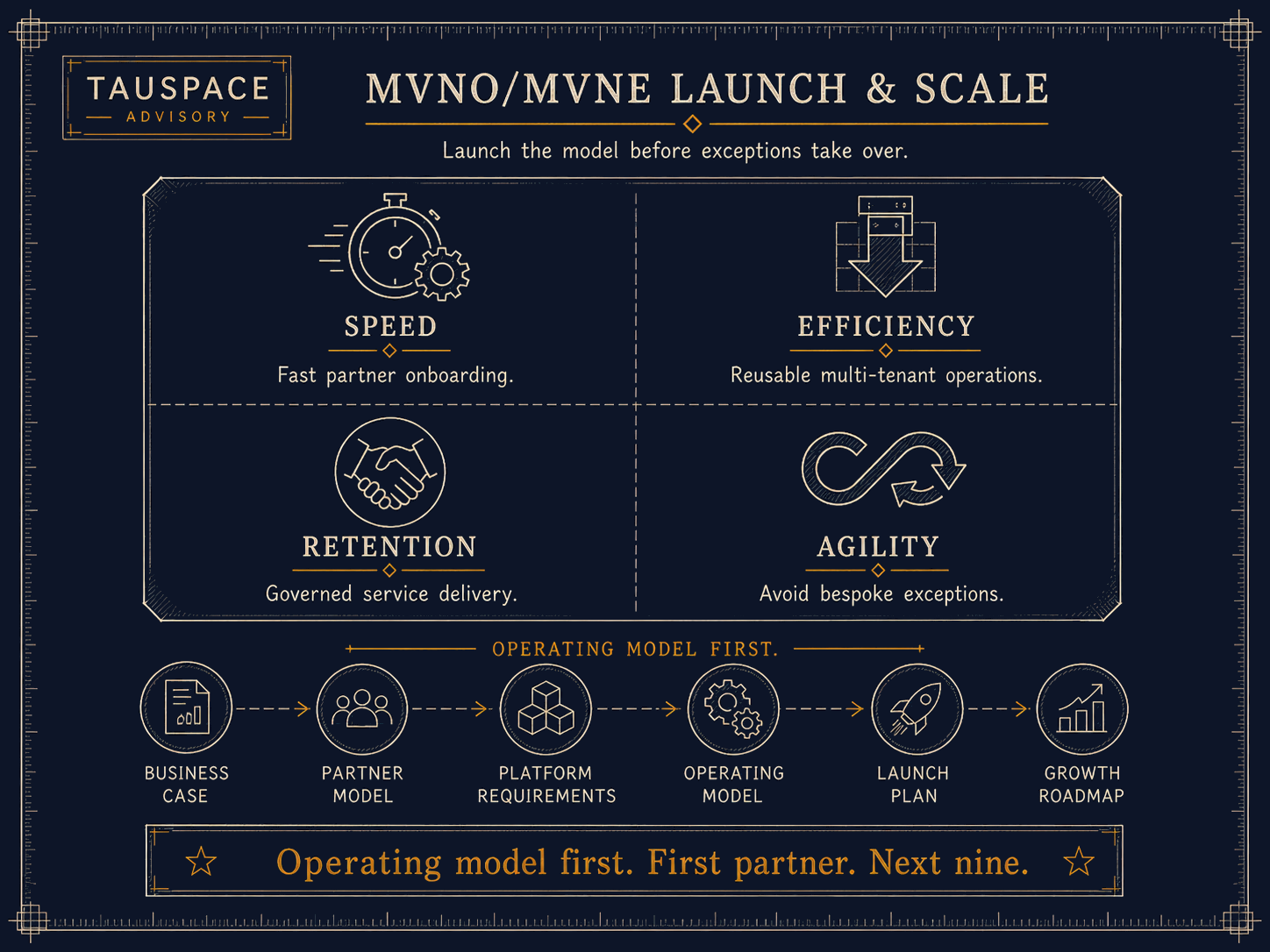

Launch the brand without building the operating mess by hand.

An MVNO or digital brand needs speed, but not at the cost of operational control. The hard work starts the day the launch goes live, when every deferred question shows up at once: who owns the customer record, where offers get evaluated, how recharge clears, who handles the partner exception that wasn’t in the model.

Questions on the table

- How fast can we launch without building a fragile operating model?

- Can we manage products, customers, offers, and partner dependencies from one operating view?

- How do we avoid leakage between the host network, digital channels, payments, and customer care?

- Can the model support growth after launch, not just the launch event?

- What needs to be handled by the platform and what needs to be handled by the operating model?

What the platform carries

What the brand team plugs into is one operating path: digital BSS, product configuration, charging, customer value, channel integration, control evidence. One spine, not six. The point is to take the disconnected decisions that usually surface after launch and put them where the business can see them on day one: who owns the customer record, where offers are evaluated, how recharge and advances clear, who handles the exceptions, and how the business proves revenue is complete.

Related advisory

Bank MVNOs

A bank MVNO needs control, not a SIM wrapper.

A bank MVNO is not only a telecom launch. It puts a new operating surface in front of customer trust, audit, risk, finance, and product. Every one of them has to be able to trust what they see, on the same evidence the rest of the bank already runs on.

Questions on the table

- How do we launch mobile without creating an ungoverned telecom operation inside the bank?

- Where do revenue leakage, settlement gaps, and control weaknesses show up?

- Can mobile support loyalty, inclusion, and customer value without becoming disconnected from banking operations?

- How do we show evidence to finance, risk, audit, product, and operations?

- What should be platform-led, and what should be handled through advisory and assurance?

What the platform carries

The Bank MVNO path runs through the Bank MVNO Suite, fullCIRCLE NEXT, Advance.ME, CVM, and revenue assurance, tied together by the control discipline the bank already runs on. The platform side carries product, customer, charging, recharge, advances, treatment decisioning, partner integration, and the audit evidence finance and risk will ask for before they ask twice.

Platform paths

MVNEs and Wholesale Businesses

More partner brands should not mean more operational drift.

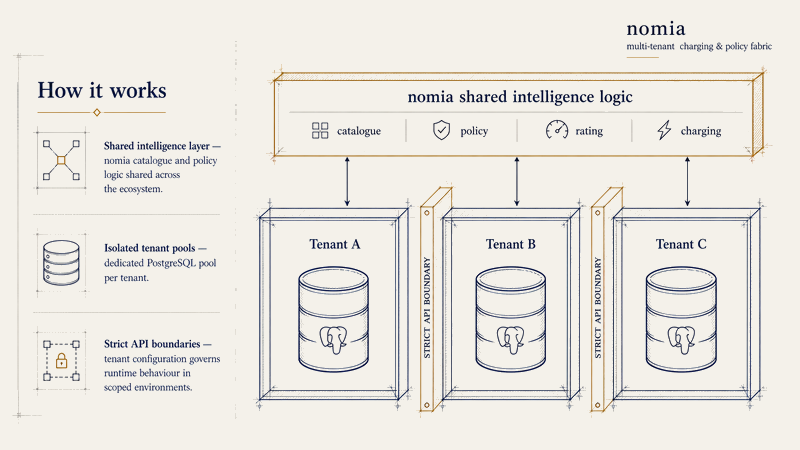

Wholesale enablement is not the same problem as launching one retail brand. The host has to give every partner the flexibility the deal promised, without rebuilding the operation each time a new brand signs, and without losing the one view across all of them the business depends on.

Questions on the table

- Can we onboard partner brands faster without building a custom stack each time?

- Can tenants, products, pricing, charging, reporting, and settlement stay separated and controlled?

- How do we support retail and wholesale operations in one operating fabric?

- Can we expose enough capability to partners without exposing the wrong controls?

- What breaks when partner growth outpaces the operating model?

What the platform carries

What sits beneath the wholesale book is multi-tenant by design: charging, digital BSS, integration, partner operations, and the operational evidence the host operator needs to keep one view across every brand. The work it lifts off the team is the rebuild-per-partner motion. Every new tenant slots into the same product boundaries, tenant rules, settlement, and service responsibilities the host already runs.

Related advisory

ISPs and FWA Operations

FWA growth exposes every weak joint in charging, care, and product control.

FWA and ISP growth can look simple from the outside: acquire customers, activate service, bill or recharge, support usage, keep the network performing. Inside the business, every one of those steps quietly multiplies into bundles, throttling rules, device flows, dunning, partner channels, and service exceptions. The operating cost of FWA is the management of those multiplications.

Questions on the table

- Can we support prepaid, subscription, hybrid, and usage-led models without custom work for every product?

- How do we handle service activation, throttling, policy, recharge, and customer treatment consistently?

- What happens when FWA grows faster than the billing and care processes around it?

- Can we launch new bundles or segments without creating manual work in operations?

- How do we see revenue, usage, care, and service exceptions early enough to act?

What the platform carries

On the FWA side, the platform brings the charging discipline operators already use (real-time rating, configurable product, policy that scales with usage), together with the customer-value, integration, and deployment support that lets a fixed-line business carry wireless without inventing a parallel operation. The goal is to take the business past the launch use case into a service operation that can actually be governed.

Channel and Enterprise Enablers

Stop making every channel deal a custom operation.

Enterprise and channel-led telecom models can easily become a series of exceptions: custom contracts, custom ordering, custom service rules, custom reporting, and manual partner support. Growth becomes expensive when every route to market needs a new operating pattern.

Questions on the table

- Can we support channel and enterprise propositions without rebuilding the process every time?

- How do we manage service packaging, partner visibility, commercial rules, and fulfilment boundaries?

- Can the platform support repeatability without removing commercial flexibility?

- Where do channel controls, service accountability, and revenue evidence sit?

- What needs to be productised before the channel can scale?

What the platform carries

What turns custom channel work into something that runs twice is one digital BSS spine: service enablement, partner operations, integrations, product configuration, and the evidence the channel is actually performing. The repeated commercial patterns become reusable instead of bespoke; the second deal of the same shape doesn’t need the second build.

Platform paths

Related advisory

When the platform path needs advisory around it

Most platform programmes fail before the platform decision.

Most platform programmes do not fail because a single feature is missing. They fail when the business case, migration path, operating model, controls, partner terms, and delivery governance are not ready for the platform decision.

TAUSPACE advisory can support the work before, during, and after platform change: strategy and business case, BSS/OSS migration, operating model, programme assurance, risk and revenue assurance, commercial advisory, and launch readiness.

Talk to us about the right path.

Tell us where the operation is under pressure and we’ll show you the platform path, the advisory work around it, and the suites or modules that carry the load.